For many drivers, “full coverage” is a safety net. Pay your premiums on time, drive carefully, and if something goes wrong, your insurer will make it right.

But for a worrisomely increasing number of policyholders across the nation, the reality check is brutal. Take this South Florida couple, for instance.

A minor crash turned into a bruising battle over whether their beloved convertible would be declared a total loss.

A Routine Crash Turns Into a Claims Nightmare

The story, first reported by CBS News Miami, begins with Patricia Heiden and Barry Rebibo, retirees in their 70s.

After Thanksgiving, Rebibo was driving their 2007 Lexus hardtop convertible along Interstate 95 when trouble struck. While the investigation doesn’t mention the exact model, the 2007 Lexus hardtop convertible is the Lexus SC 430.

The collision left the car with a punctured front tire and a damaged bumper. It was frustrating, yes, but hardly catastrophic. If not for the flattened tire, Rebibo believed he could have driven the car home.

Confident in their coverage, the couple contacted State Farm. They had what they describe as full coverage, paid their premiums faithfully, and expected a straightforward claims process. Instead, they say they ran into silence. Calls were not returned.

When they finally reached someone, it was not a routine claims adjuster on the line but the insurer’s total loss department.

And that is where their story took a shocking twist that’s quickly becoming all too familiar with car owners in America.

Fighting for Answers

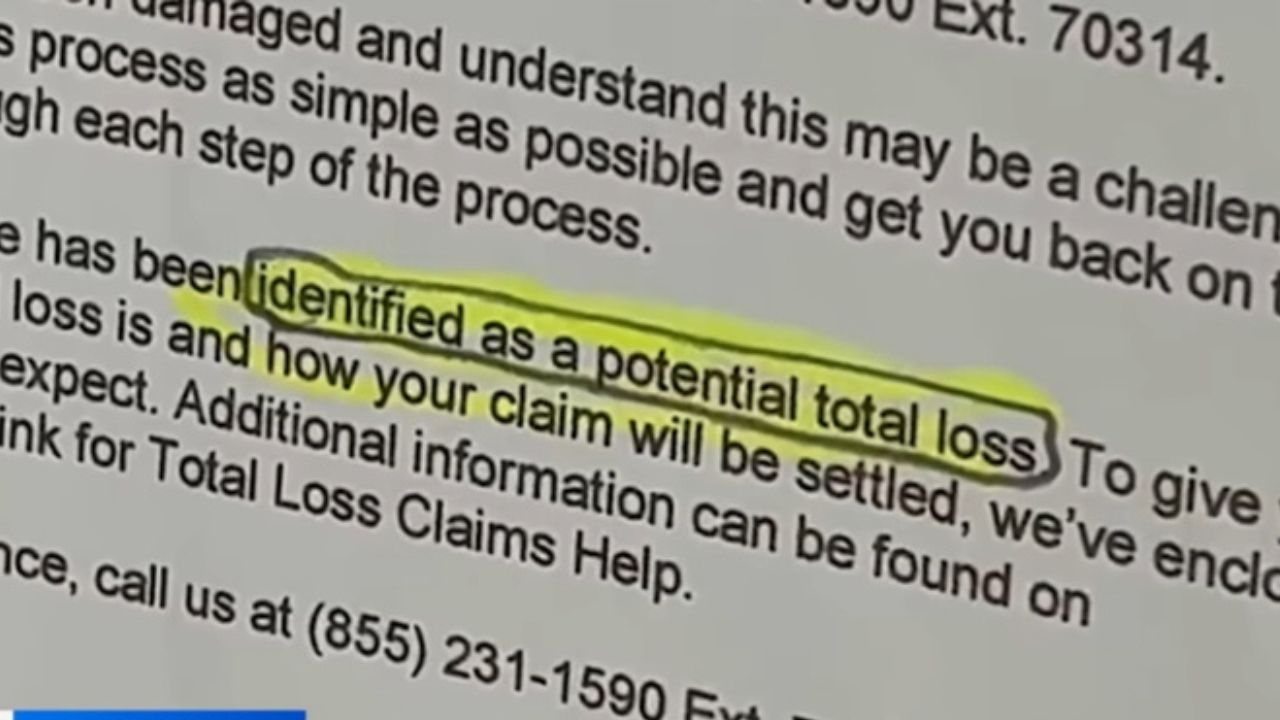

According to the couple, State Farm informed them that the Lexus had been declared a total loss. The determination, they were told, was based on an assessment connected to a body shop.

Heiden and Rebibo asked for paperwork explaining how that conclusion was reached. They say they were met with resistance and increasingly tense conversations.

At one point, they claim a representative grew aggressive and even threatened to hang up when they refused to accept the decision without documentation.

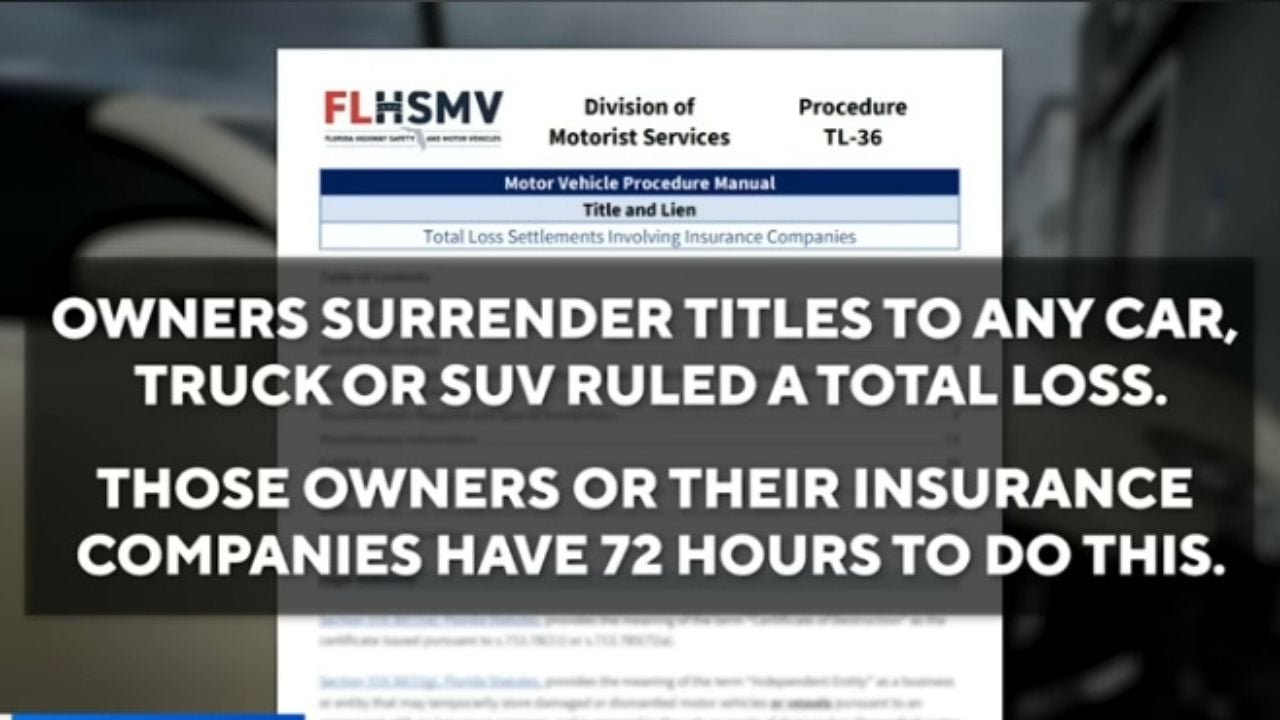

Under Florida law, once a vehicle is officially ruled a total loss, the owner must surrender the title within 72 hours. Owners can opt to buy back the vehicle with a salvage title, but that comes with restrictions on how the vehicle can be driven or sold.

For many drivers, that designation can effectively end a car’s usable life.

The stakes seem rather high for the car owner. Rebibo’s 2007 Lexus may be old, but it has obviously lasted that long because it was a well-maintained convertible that still had life left in it, at least in the couple’s view. To keep it in service for that long shows they cherished the car. Giving it up over what appeared to be moderate damage felt premature.

The SC 430 was a 2-door luxury hardtop convertible powered by a 288-hp 4.3L V8, mated to a 5-speed automatic transmission. In 2007, Lexus offered the SC 430 in a single well-equipped trim level (no multiple trims like “Base” vs. “Sport”), with standard luxury features such as leather upholstery, navigation, and premium audio.

When pressed for comment by CBS News Miami, State Farm declined to discuss the specifics of the claim, citing customer privacy policy.

The Economics of Total Loss

Consumer advocates say situations like this are not rare. Michael DeLong of the Consumer Federation of America explains that with older vehicles, even relatively minor crashes can tip the scales toward a total loss declaration.

Insurance companies calculate whether repair costs exceed a certain percentage of the car’s market value. Because older cars have lower valuations, it does not take extensive damage to reach that threshold.

DeLong advises drivers to seek an independent opinion. Insurers often direct customers to preferred adjusters or partner body shops. While that does not automatically mean the evaluation is flawed, a second inspection can provide clarity and leverage if there is disagreement over repair costs.

Heiden took that advice seriously. A retired psychotherapist familiar with insurance claims, she meticulously documented everything. She kept a binder filled with receipts, emails, text messages, and even detailed logs of phone conversations.

According to her notes, a supervisor later admitted that the total loss designation had been made before any mechanic had physically examined the car.

A Hard-Fought Victory and a Cautionary Tale

Three months after the crash, the couple was allowed to pursue an independent inspection. The result changed the trajectory of the case. The new repair shop estimated it could fix the Lexus for roughly half of State Farm’s original estimate. Ultimately, the insurer agreed to cover the repairs.

It felt like a victory, but not a clean one. The couple described the process as an unnecessary battle that no policyholder should have to fight.

There is a cautionary note here. Pushing back does not always lead to a favorable outcome. Insurers may stand firm, prolong negotiations, or even escalate disputes to court. Still, drivers who believe they are being treated unfairly have options.

In Florida, complaints can be filed with the Florida Office of Insurance Regulation, the agency tasked with protecting consumers.

This couple’s experience with State Farm can serve as a wake-up call for people who own and/or insure older cars. A minor accident can quickly become a major financial crossroads because the insurer tends to dodge a payout that exceed a certain percentage of the car’s market value.

Knowing your rights, documenting every interaction, and seeking independent assessments could mean the difference between surrendering your keys when you don’t want to.

Note: This article contains embedded video. Embedded media may not display on all platforms. The video is available on our website here.

This has happened to us twice with State Farm. We had a Porsche Macan that was a 2017 and they totalled the vehicle as the front end had damage and tried to give us a lower price than it was worth…I always save my window sticker as proof of what the car has as they try to rip you off…insisting it doesn’t have the upgrades. They did the same thing on a new car for a fender bender as they wanted us to use their affiliated body shop (which just means they rip them off too). We couldn’t as our car had a matte finish and their body shop had us move the vehicle to one that could do the matte finish. It took a month and a half of rudeness by their claims people for us to agree for them to total the car at a much higher price than originally offered. Never accept their first offer. We changed insurance companies after as they have become the worst! We had been with State Farm for 50+ years with no accidents.

Most people have a poor opinion of State Farm and a few others.