A troubling trend is emerging in the auto finance world, and it is hitting drivers where it hurts most. Across the United States, auto loan defaults have surged to their highest level in over a decade, with nearly three million vehicles repossessed in the past year alone.

The spike reflects mounting financial pressure on households grappling with inflation, rising living costs, and tightening credit conditions.

In Colorado, the situation is drawing particular attention due to a controversial aspect of state law. Currently, lenders can repossess a vehicle after just one missed payment. Even more alarming for many consumers is the growing use of remote disabling technology. This allows dealerships or lenders to shut down a car electronically, sometimes without warning.

A Terrifying Incident on the Highway

That is exactly what happened to one driver, Duffy Fraser. While rushing her son to the hospital on Interstate 25, she says her vehicle suddenly locked up. The steering wheel froze, the hazard lights failed, and she was left stranded in active traffic.

Initially, it was a terrifying mechanical failure. But then her terror turned into outrage when she eventually learned the truth. The dealership had remotely disabled her car because she had missed a payment.

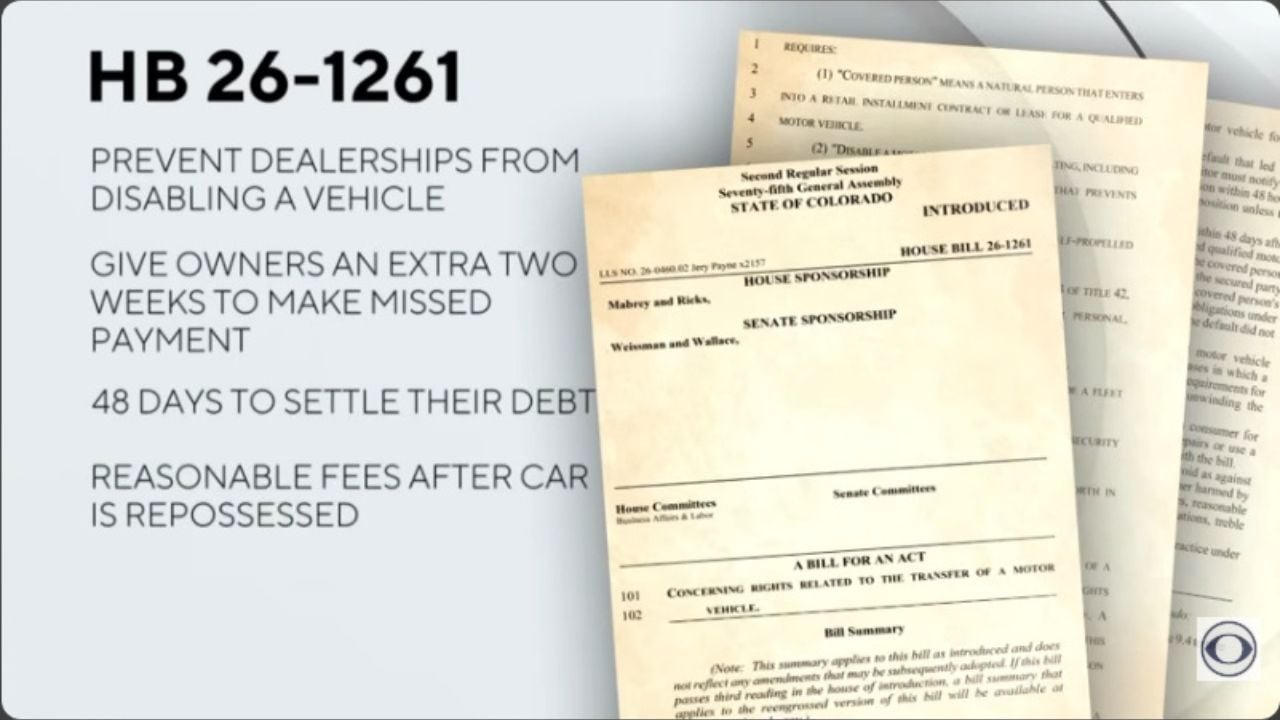

Stories like Fraser’s are fueling a push for reform. State Representative Javier Mabrey has introduced a bill aimed at giving consumers more breathing room and protecting them from sudden repossessions or dangerous remote shutdowns. His proposal would prevent dealerships from disabling vehicles remotely and extend the grace period for missed payments.

Under current rules, borrowers typically have about 20 days before repossession can occur. Mabrey’s bill would extend that timeline, giving consumers up to 48 days to settle their debt and associated fees. It would also impose stricter penalties on lenders who violate the rules, classifying such actions as deceptive trade practices with the possibility of triple damages.

A Debate Over Consumer Protection

Many in the state feel these changes are long overdue. Missing a single payment, they say, should not trigger consequences that can cascade into job loss, financial ruin, or even life-threatening situations. For many Americans, a car is not a luxury but a necessity for getting to work, accessing healthcare, and supporting their families.

However, the proposal is facing strong opposition from industry groups. Organizations like the Colorado Auto Dealers Association warn that the bill could create confusion and increase costs for lenders and dealerships.

According to spokesperson Matthew Groves, the legislation introduces vague language around what constitutes “unreasonable fees,” potentially exposing businesses to years of legal disputes.

Critics also argue that the financial burden of delayed repossessions could shift risk back onto lenders, affecting interest rates and credit availability for future buyers. They caution that the proposal might come across as consumer protection but ultimately make auto loans more expensive or harder to obtain.

Additional Provisions and Uncertain Future

Beyond repossession rules, the bill includes additional consumer-friendly measures. It would allow used car buyers to return them within three days for a refund, creating a short window for reconsideration after purchase. It also seeks to limit charges for excessive mileage or repairs deemed unreasonable.

Still, opponents say reversing a vehicle purchase is not simple. It can involve untangling title transfers, warranties, service contracts, and trade-in agreements, all of which add layers of complexity and cost.

In the meantime, the future of Mabrey’s bill remains uncertain. As it heads to committee review, lawmakers must weigh two competing realities. On one side are consumers struggling to stay afloat in a challenging economy. On the other are financial institutions and dealerships concerned about operational risks and legal exposure.

What is clear is that the conversation around auto lending practices is shifting. As technology gives lenders more control over vehicles and economic pressures push more borrowers to the brink, the balance between consumer protection and industry stability is being tested like never before.