A Michigan driver says she lost more than $8,000 after her insurance company initially approved her claim for a totaled vehicle and later reversed its decision. Her story got people online talking and asking questions about loopholes in state insurance rules.

The case involves Novi resident Aisha Moore, who believed she had done everything right after buying a policy from CURE Auto Insurance in November 2023. According to Moore, she paid her premium every month and expected the coverage to protect her if an accident ever happened.

That accident came in April 2024.

A Total Loss, Then a Reversal

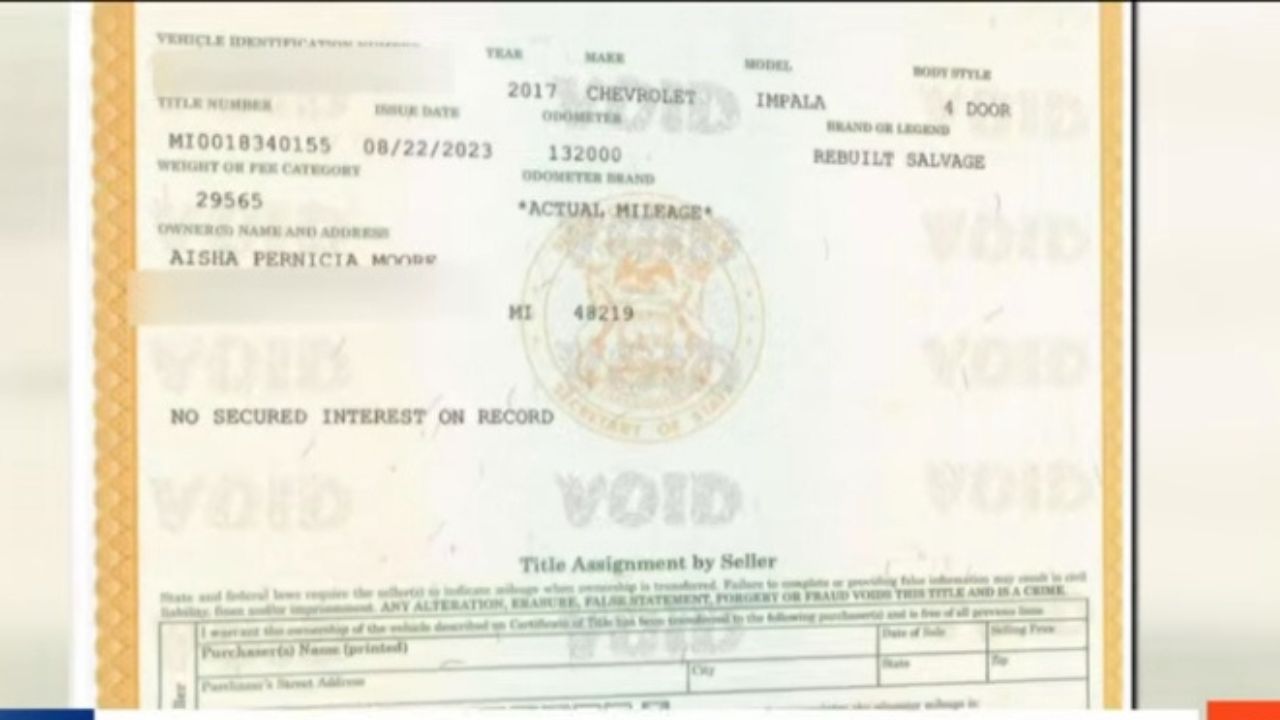

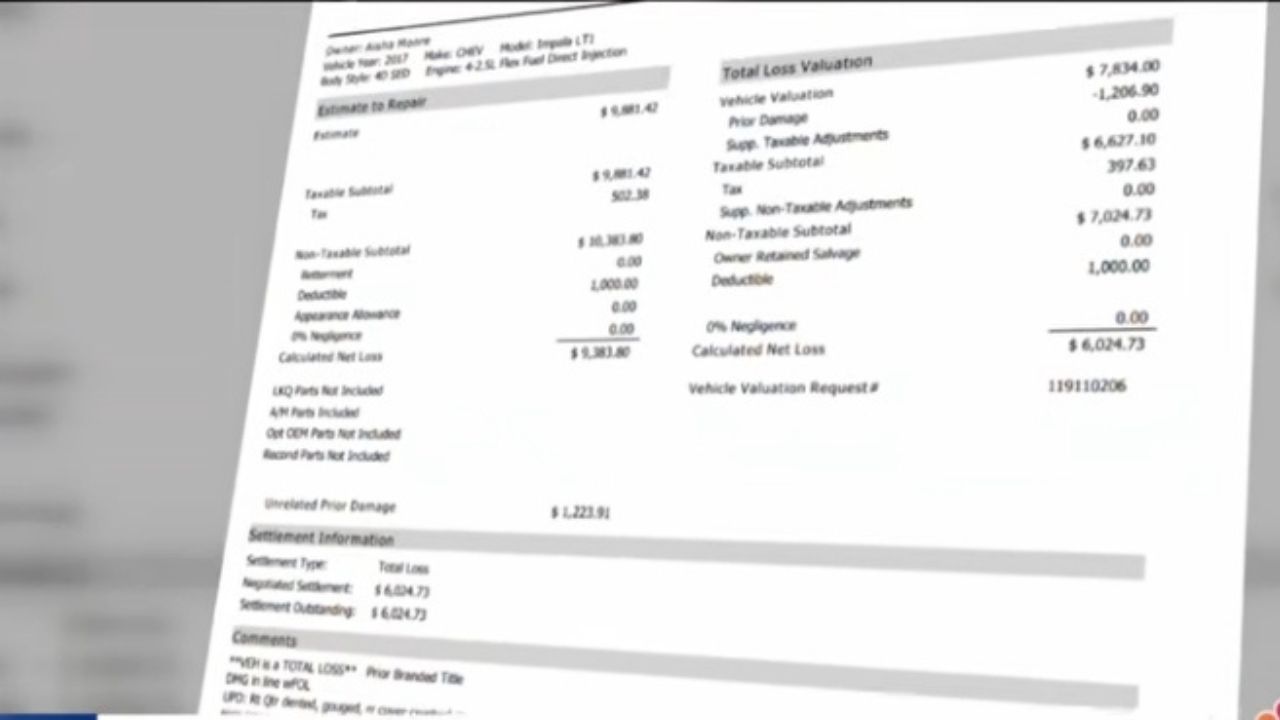

Moore’s vehicle was badly damaged in the crash, and the insurance company later declared the car a total loss. Under normal circumstances, once a vehicle is declared totaled, the process is straightforward. The vehicle owner transfers the title to the insurance company and receives payment equal to the car’s actual cash value.

Moore says she followed that process.

Her attorney, Lawrence K.G., explained that Moore signed over the title to the insurer as required after the total loss determination.

But what happened next raised serious concerns.

According to the attorney, the insurance company transferred the title of Moore’s vehicle on August 9, 2024 to an auto parts store in Michigan, suggesting the vehicle had already entered the salvage pipeline. Typically, once the insurer takes ownership of a totaled car, it may be dismantled for parts or sold through salvage auctions.

Yet months later, Moore says she still had not received payment.

A Disputed Household Member

Then, in October 2024, the situation took a dramatic turn.

Instead of issuing compensation for the totaled vehicle, the insurer sent Moore a notice claiming that her policy was invalid. The company alleged that she failed to disclose a person living in her household when she applied for coverage.

The person in question was reportedly her brother’s girlfriend.

Moore strongly disputes the claim. She insists the woman did not live with her at the time she signed up for the insurance policy.

Her attorney says the denial came after multiple attempts to collect payment from the insurer.

He claims the company not only refused to pay for the totaled vehicle but also kept the proceeds from the car after it had already transferred the title and sold it for parts.

Seeking answers, reporter Kyla Russell contacted the company’s leadership.

The CEO of CURE Auto Insurance said he could not discuss specific details about Moore’s case because she had not signed a consent waiver allowing the company to share information.

However, he did provide a general explanation of how insurance companies evaluate household information.

Why Household Details Matter

According to the insurer, applicants are required to disclose everyone who lives in their household. The company said it has recorded statements that contradict Moore’s claim about who was living in the home at the time.

Insurance companies place significant importance on household members because it can affect risk calculations.

Even people who do not drive a vehicle may influence insurance pricing. Insurers often consider all residents when determining rates because any licensed driver in the household could potentially access the insured vehicle.

As such, it’s easy to see how this practice can lead to disputes and claim denials if household information is incomplete or interpreted differently by the insurer.

For Moore, the dispute has left her without the payment she expected after losing her car.

Her attorney says cases like this are not uncommon. He claims that lawsuits against insurers over denied claims often succeed when policyholders challenge the decision in court.

We once reported the story of a family, also in Michigan, that got denied by GEICO because they hadn’t notified the insurer when the family got a new member — their three-month-old baby.

According to the law firm representing Moore in this case, it has recovered benefits in more than 90 percent of cases where an insurer initially denied a claim.

A Lesson for Policyholders

Meanwhile, lawmakers in Michigan are beginning to take notice of cases like Moore’s.

The controversy has drawn attention to a proposed legislative measure, Michigan Senate Bill 782, which aims to address gaps in state law related to insurance claims and policy disclosures.

This story spotlights a critical lesson for car owners. When applying for auto insurance, accurately listing every household member can be just as important as paying the monthly premium.

And when disputes arise, legal experts say policyholders should not assume a denial is the final word.

Editorial Note: Video playback may be limited or restricted on certain platforms. If you are unable to watch the video here, please visit our main website and search the article’s title, where full playback will be available.